Managing Debt | Personal Finance | Article

How to Clear Debts Fast

by The Simple Sum | 29 Sep 2020

One moment someone’s paying for groceries with a credit card, and the next thing they know – after a few forgotten payments – they are saddled with $50,000 in debt.

Sounds extreme? Maybe not. Debts can easily arise from bad financial habits. But it can even arise when bad luck strikes – from losing a job or falling gravely ill.

To tide over a rough patch, one might be tempted to take out a loan or rely on a credit card. After all, it’s just temporary; things will get better! But sometimes, things don’t improve. Then debt starts compounding. Then it snowballs out of control.

So, the nightmare begins.

The red letters demanding repayments start to pile. By then, it can seem like there is no way out. If you find yourself in this situation, don’t lose hope. Here are some strategies to help manage debts that seem out of control.

Managing Your Web of Multiple Credit Lines

A common problem faced by debtors is the complexity of juggling multiple payments. Needless to say, the main priority is to clear these debts fast, before the accrued interest gets higher and higher.

There are two common methods to tackle multiple debts:

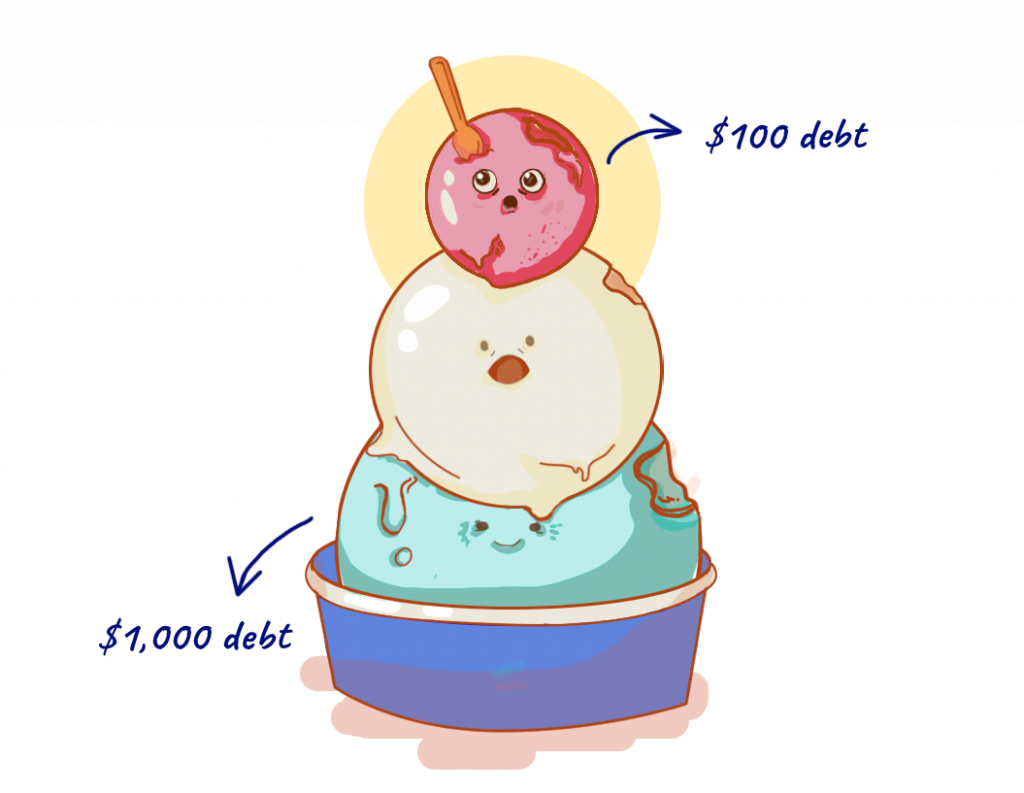

Snowball Method

- Pay the minimum sums* for all debts

- List out existing debts in order from smallest to largest

- Put the remainder towards the smallest debt to clear it off, and continue onto the next smallest debt

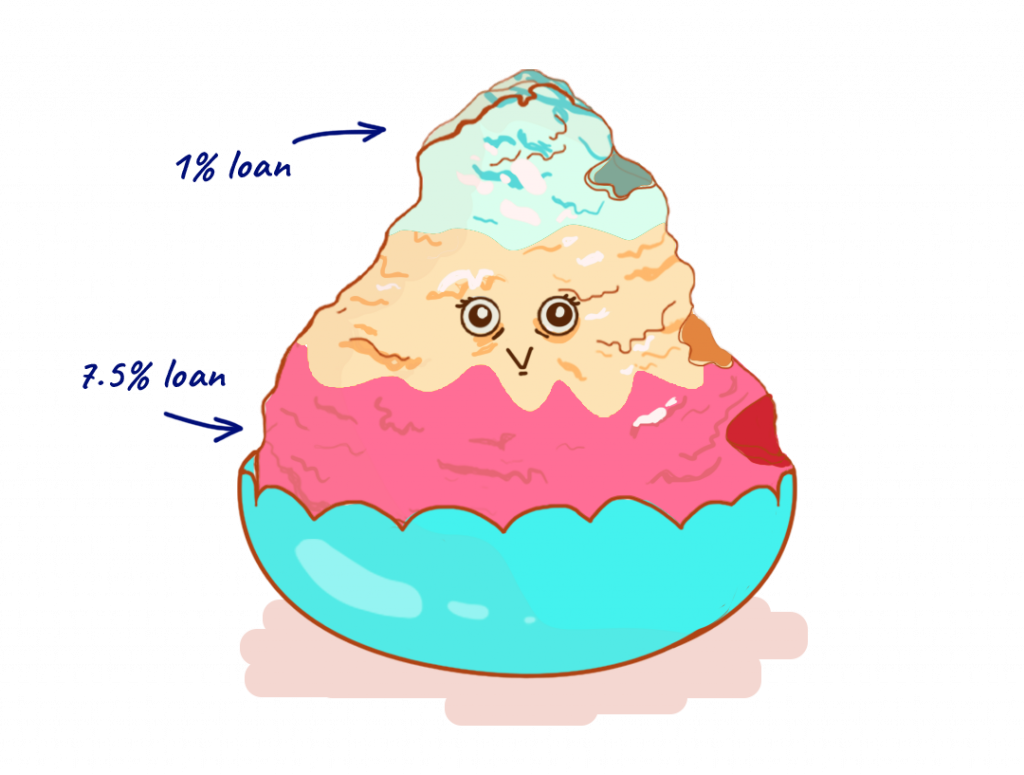

Avalanche Method

- Pay the minimum sums for all debts

- List out existing debts according to interest rates from largest to smallest

- Repay as much as is possible for the debt with the largest interest rate, before moving on to the next one and so on

*minimum amount possible that reduces some debt principal

Both methods place an importance on first paying off the minimum sums for each debt, so some of the principal (original amount loaned) is being chipped away, preventing the debt from growing bigger.

But more importantly the methods help debtors list and take stock of their debt situation, and provides a simple action plan to keep a debtor focused on clearing off their debts.

We have some recommendations between these two methods.

- The Avalanche method is better suited for those who are struggling with credit card debt in addition to low-interest or smaller loans. By dealing with the higher interest loan first, no snowballing will occur – and the loan is settled in a shorter period of time, thus incurring lesser interest.

- The Snowball method can be used for low interest or smaller loans, whether it’s a personal loan from family or overdue bills towards telcos or utilities. This is a systematic way of handling loans and bills in an organised way, without neglecting any by accident.

But When It All Seems Too Much

But what if a debtor can’t even pay off the minimum sums for all their bills? Perhaps they lack personal finance fundamentals – such as budgeting – so they find it hard to find the money to make consistent repayments.

In that case, there are several banks in Brunei that provide schemes to help them manage multiple loans by consolidating their outstanding balances into a single loan.

Consolidation Financing Scheme (BIBD) and Consolidation Loan (Baiduri)

Eligibility Requirements

- Employee of Brunei Government, Semi-Government and private sector companies accepted by the Bank

- Existing Total Debt Servicing Ratio (TDSR)* must exceed 60%

- Only financing facilities that were granted before 8 June 2015 and under the name of the Applicant are allowed to be consolidated

- The final entitlement shall be subject to the banks’ internal credit policies and assessment

*TDSR refers to the portion of the borrower’s monthly income dedicated to paying off debt

Consolidation Loan (Standard Chartered)

Eligibility Requirements

- Brunei citizens, permanent resident or expatriates

- Age: 21 to 60 years old

- Valid employment contract and employment pass (for expatriates)

What happens if you can’t resolve your debt?

If a debtor is unable to repay their loans even after utilising the banks’ consolidation plan, this is where a third party agency will step in. Usually this will involve the agency sending Letters of Demand to the debtor requesting repayment. If the debtor is still unable to resolve their debt, they will be brought to court.

In the end no mountain is insurmountable – even one made out of debt. For borrowers who are beginning to find themselves in trouble, it is not the end. With every step in the right direction (and a whole lot of discipline and transparency), a debt-free life is possible.